When the Money Itself Is the Transition

On debt cycles, elite overproduction, and what happens when the financial architecture of an era reaches the limits of its own logic

The previous essay in this series introduced the S-curve as the structural path that technological revolutions follow through productive economies. The argument was that every major technological paradigm moves from installation through crisis through deployment, and that the most dangerous position for an institution is the overlap, the period of confident optimization for a world that the structural horizon has already identified as ending. That argument is about technology. It is about how new productive capacities displace old ones and what happens to the institutions built for the paradigm that is saturating.

This essay is about something different. It is about the financial architecture that sits underneath the technology story, the systems through which capital is created, allocated, concentrated, and eventually either redistributed or destroyed. Capital does not follow an S-curve. It does not move from installation through deployment toward productive maturity. It follows a different path entirely, one that is older than any of the technological paradigms we have examined, one that has been documented across centuries and across civilizations, and one that has arrived, by the account of several of the most rigorous analysts working in this space, at a particularly consequential point in its own long cycle.

Understanding that path does not require a background in economics or finance. It requires only a willingness to look at the financial system not as background infrastructure, the water in which economic life swims, but as a historical artifact with its own internal logic, its own structural vulnerabilities, and its own predictable patterns of expansion and crisis. When you look at it that way, the current moment becomes legible in ways that the technology story alone cannot produce.

The long cycle that most planning ignores

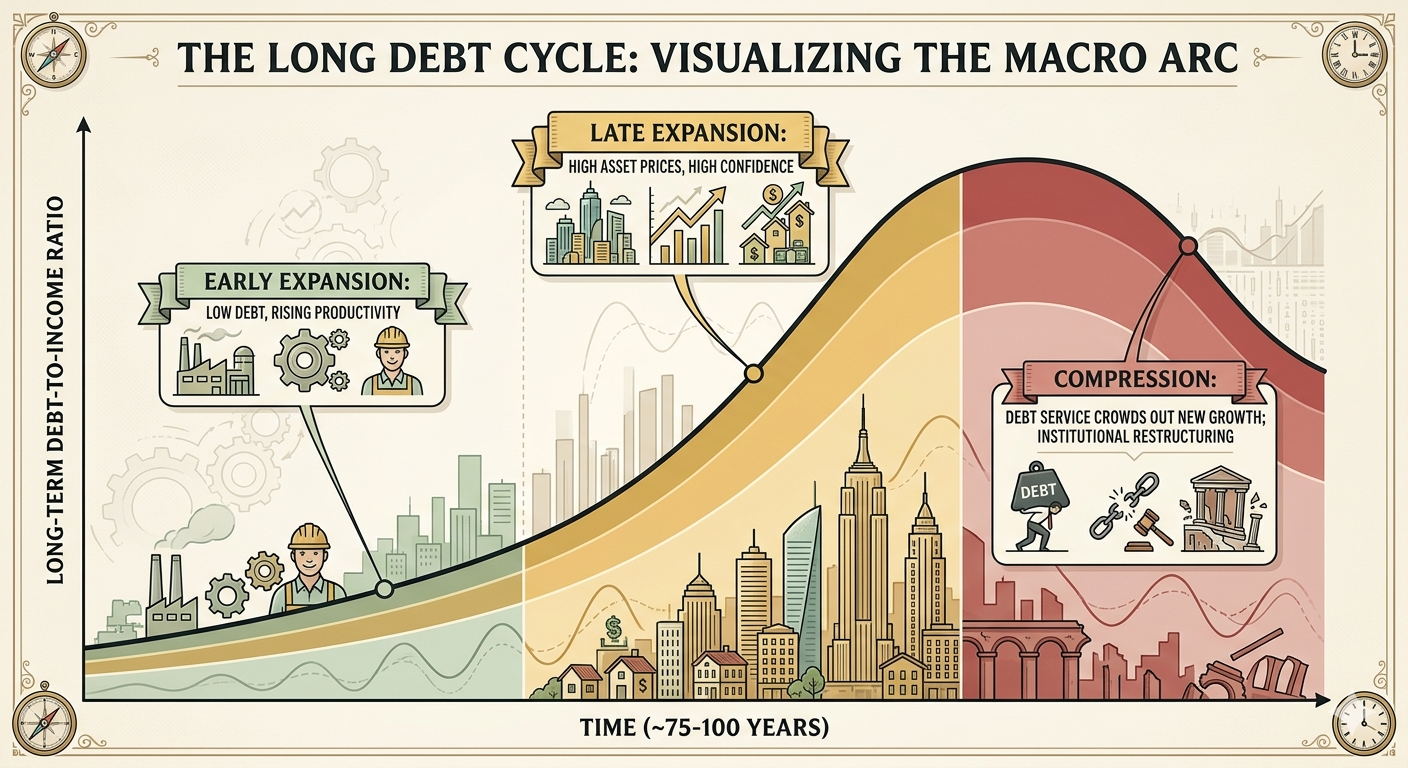

Ray Dalio spent decades building one of the most successful investment firms in the world, and a significant part of what distinguished his approach was a willingness to study financial history at timescales that most practitioners consider irrelevant to operational decision-making. The result of that study is a framework he calls the long debt cycle, and its core argument is straightforward enough to state in a few sentences even though its implications take considerably longer to absorb.

In the short term, economies move through business cycles of roughly 5 to 10 years, expansions followed by recessions, periods of credit growth followed by periods of deleveraging. Most institutional planning is calibrated to this cycle, because it is the one that produces the quarterly and annual fluctuations that feel most immediately consequential. But beneath the short cycle, Dalio argues, there is a longer one, running approximately 50 to 100 years, in which the total level of debt in an economy, relative to income, rises steadily over generations until it reaches a structural limit.

The mechanism is not complicated. Credit allows economic actors, individuals, corporations, and governments, to spend more than their current income by borrowing against future income. When credit expands, economic activity accelerates, asset prices rise, and the experience of participants is one of general prosperity and institutional confidence. The expansion is self-reinforcing for a long time: rising asset prices make collateral more valuable, which allows more borrowing, which pushes asset prices higher. Each generation that comes of age during the expansion experiences the credit system as a natural feature of economic reality rather than as a historical artifact, and builds its institutional assumptions accordingly.

The limit arrives when the ratio of debt to income reaches a level at which servicing the existing debt consumes so much of current income that new borrowing can no longer generate the economic activity needed to service the old borrowing. At that point the long cycle enters its compression phase, and the compression is not a brief recession of the kind the short cycle produces. It is a prolonged and structurally different kind of reckoning, one that reshapes the financial architecture of the era in ways that cannot be managed through the tools designed for short-cycle management.

Dalio's examination of historical long debt cycles, including the one that ended in the Great Depression and the one that ended various European imperial financial systems in the early twentieth century, produced a consistent observation: long debt cycle compressions are not primarily economic events. They are institutional events. They reshape the relationship between creditors and debtors, between financial institutions and the governments that regulate them, between the holders of financial assets and the holders of productive assets, in ways that require new institutional frameworks rather than simply the repair of existing ones. The compression does not restore the previous equilibrium. It produces a new one, and the character of that new equilibrium is determined by the political and social choices made during the transition rather than by any automatic economic mechanism.

Dalio places the current moment near the end of a long debt cycle that began in the aftermath of World War II. The total debt levels, public and private, relative to productive income, across the major economies that have organized the postwar financial architecture have been rising for decades and have now reached levels that have historically preceded long cycle compression events. This does not mean a specific crisis is imminent on a specific date. It means that the financial architecture of the postwar era is operating under structural stress that the short-cycle tools of monetary and fiscal policy can manage in the near term but cannot resolve at the structural level, because the problem is not a short-cycle problem.

The social consequence of where the cycle has arrived

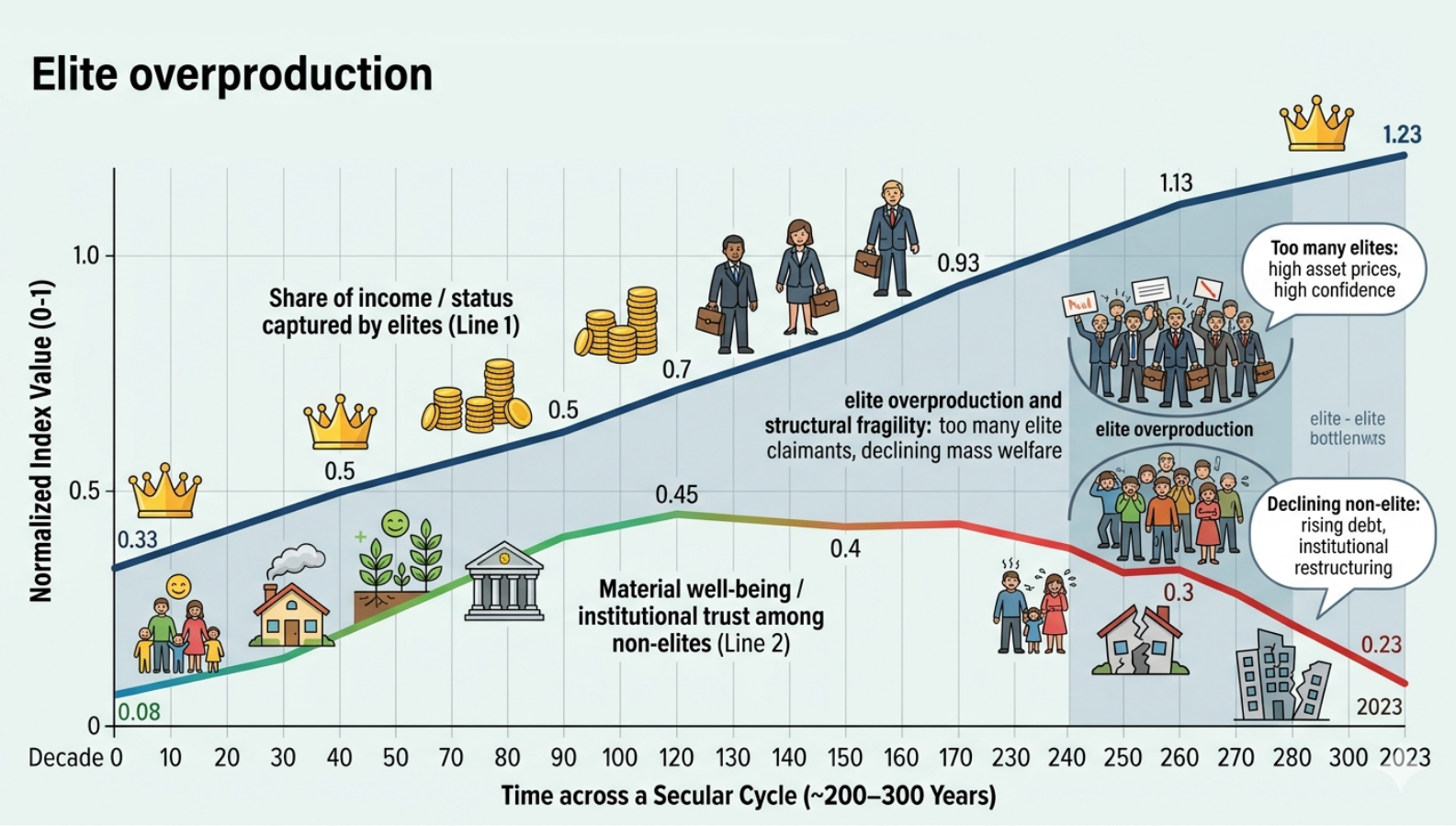

Peter Turchin came to the study of historical cycles from a background in ecology and mathematical biology, which gave him a set of analytical tools that historians and economists rarely apply to social systems. His central argument, developed over two decades of quantitative historical research, is that societies move through secular cycles of roughly 200 to 300 years, and that within those cycles there is a predictable pattern connecting the distribution of wealth to the stability of institutions.

The mechanism Turchin identifies is what he calls elite overproduction. In the early phases of a secular cycle, when productive capacity is growing and wealth is being generated faster than existing elites can capture it, there is enough economic surplus to sustain both the established elite and the institutions that serve the broader population. Social mobility is real. Institutional trust is relatively high. The system feels, and largely is, capable of delivering broadly shared prosperity.

As the cycle matures and wealth concentrates, two things happen simultaneously. The established elite grows in absolute terms, producing more claimants to elite status than the economy can absorb into genuinely elite positions. And the share of economic output flowing to non-elite populations declines, eroding the material basis of the institutional trust that the earlier phase generated. The result is a society with too many people competing for too few positions at the top, increasing immiseration at the bottom, and institutions that are no longer delivering the outcomes that legitimized them.

Turchin is careful to note that this configuration does not automatically produce crisis. What it produces is structural fragility, a condition in which institutions that functioned adequately under normal conditions become brittle under stress, in which the social trust that previously absorbed shocks has been depleted, and in which the elite competition that the overproduction dynamic generates begins to destabilize the political frameworks that previously managed it. The specific form that crisis takes, when it takes a form at all, is determined by contingent factors. The structural fragility that makes crisis possible is determined by the cycle.

His quantitative analysis of American history produced a finding that is difficult to dismiss given its methodological rigor: the indicators he tracks, inequality measures, political polarization indices, measures of institutional trust, elite competition for political office, all of which he treats as empirical variables rather than qualitative impressions, have been moving in the directions his secular cycle framework predicts for the past several decades, and they are now at levels comparable to the periods immediately preceding the major American institutional crises of the nineteenth and early twentieth centuries.

Turchin is not predicting a specific outcome. He is documenting a structural condition. And that condition, viewed alongside Dalio's long debt cycle analysis, produces a picture of the financial and social architecture of the current moment that the technology story alone cannot provide: a system that has been generating inequality at the structural level for long enough that the institutions built to manage a more equitably distributed prosperity are now operating under stresses they were not designed to absorb.

The platform underneath the cycles

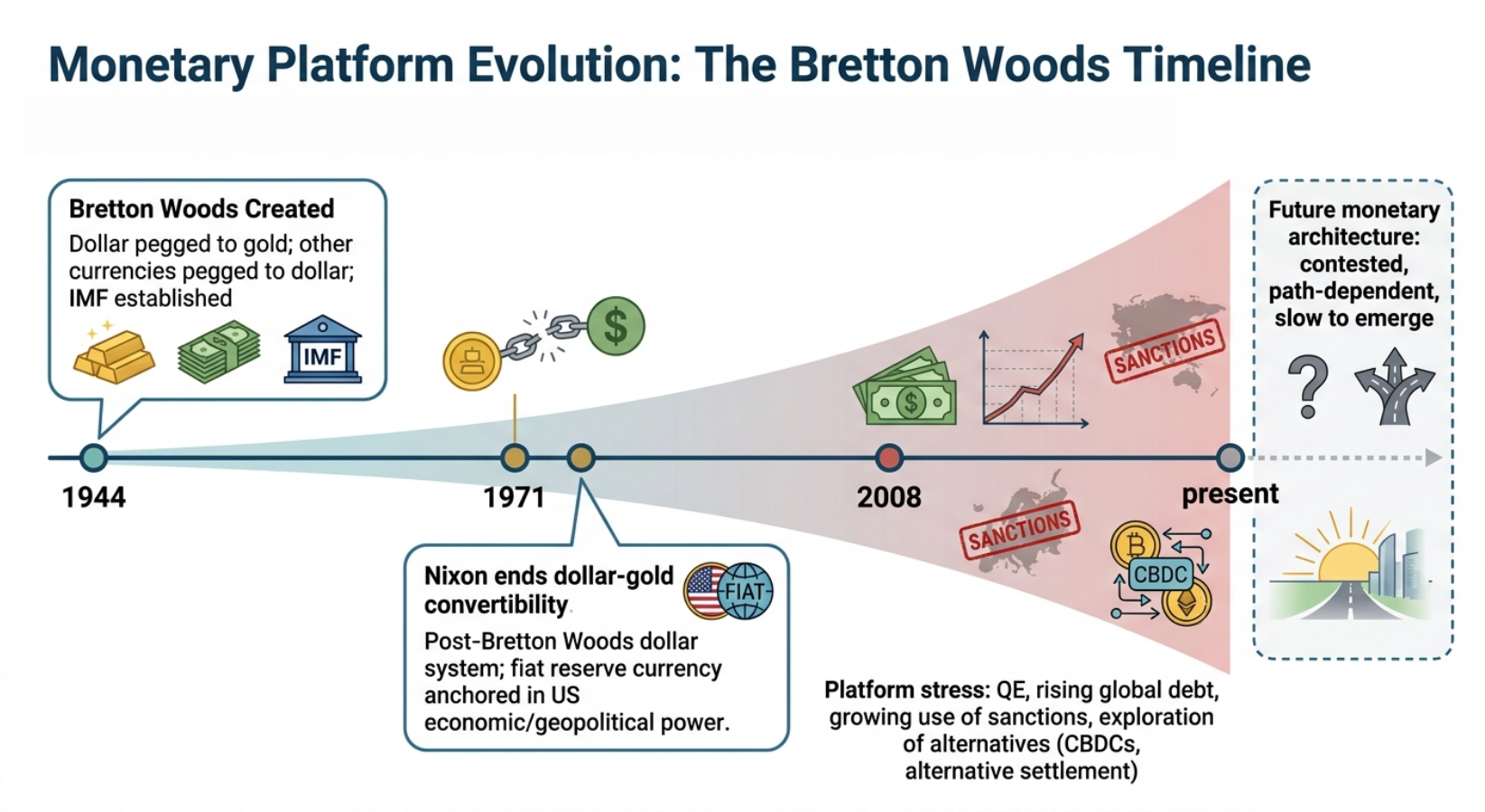

There is a third dimension of the capital story that neither Dalio nor Turchin addresses directly, and that requires its own brief treatment because it is the foundation on which both of the frameworks above rest. It is the question of monetary architecture: the specific institutional arrangements through which money itself is created, denominated, and trusted, and what happens when those arrangements face a legitimacy crisis.

The Bretton Woods agreement of 1944 established the United States dollar as the world's reserve currency, tied initially to gold and then, after Nixon ended dollar convertibility in 1971, maintained by the geopolitical reality of American economic and military dominance. The post-Bretton Woods dollar system has organized international finance for more than half a century. It has determined how global trade is denominated, how sovereign debt is issued and serviced, how central banks manage their reserves, and how the costs and benefits of financial crises are distributed across the global economy. It is not merely a policy choice. It is a platform, the operating system on which the entire postwar financial architecture runs.

Platforms of this kind do not fail the way S-curves saturate or the way cycles compress. They hold, sometimes well past the point at which the geopolitical conditions that justified them have changed, because the cost of transitioning away from an established monetary platform is extraordinarily high and no actor in the system has an individual incentive to bear that cost unilaterally. And then, when the gap between the platform's institutional form and the geopolitical reality underneath it becomes large enough, they break, and the breaking is a different kind of event than either a technological paradigm shift or a debt cycle compression. It is a crisis of monetary legitimacy, which is to say a crisis of the shared framework of trust on which all financial activity ultimately depends.

The dollar system is not broken. It remains the dominant global reserve currency and the primary denomination of international trade and sovereign debt. But it is under challenge in ways that have no precedent in the postwar era. The weaponization of dollar-denominated financial infrastructure as a geopolitical tool, through sanctions regimes and exclusions from payment systems, has given other major economies a concrete incentive to develop alternatives that they previously lacked. The rise of central bank digital currencies, the experiments with alternative trade settlement systems among major non-Western economies, the broader contestation of financial infrastructure that the current geopolitical realignment has accelerated, all of these are symptoms of a platform facing questions about its long-term legitimacy that the previous era did not generate.

This does not mean the dollar system is about to collapse or that a new monetary architecture is imminent. History suggests that monetary platform transitions are extremely slow and deeply disruptive, and that the incumbent platform retains enormous advantages long after its structural vulnerabilities become visible. What it means is that the financial architecture most institutional planning treats as permanent background is itself in a condition of structural uncertainty, and that uncertainty compounds the stresses produced by the debt cycle and the secular cycle in ways that are not yet fully visible at the event horizon but are clearly legible at the structural one.

Three cycles, one picture

The technology story and the capital story are not separate narratives that happen to be unfolding simultaneously. They are aspects of the same structural transition, and understanding their relationship requires holding all three capital dimensions together with the technological framework from the previous essay.

Technological revolutions require capital to install themselves, and the financial architecture of the era determines how that capital is allocated and on what terms. The current AI revolution is being installed under conditions of late long-cycle debt expansion, which means the speculative capital available to accelerate it is abundant but the productive economy it is accelerating into is operating under the structural stress of a system near the limits of its credit capacity. The installation period is happening in a financial environment that is simultaneously more liquid and more fragile than any previous technological revolution has encountered.

The secular cycle dynamic compounds this in a specific way. The concentration of wealth that Turchin's framework identifies as the signature of late secular cycle conditions means that the productive benefits of the current technological revolution are being captured by a narrower slice of the population than the productive benefits of previous technological revolutions were. This is not an automatic outcome of the technology itself. It is a consequence of the specific financial and institutional architecture within which the technology is being deployed, an architecture that reflects where the secular cycle has arrived rather than any inherent property of artificial intelligence or automation.

And underneath both of these, the monetary platform on which the entire system runs is facing legitimacy questions that previous technological revolutions did not have to navigate. The deployment phase of the current paradigm, whenever it arrives, will have to construct itself on a monetary foundation whose long-term architecture is genuinely uncertain in ways that the deployment phases of previous technological revolutions were not.

The reader who has absorbed the technology story and the capital story together now has a picture of the current economic transition that is considerably more complex than the S-curve alone provides, and considerably more honest about the specific character of the stresses that complexity is generating. It is not a story of disruption and adaptation, the vocabulary of business-school innovation discourse. It is a story of multiple structural systems, each with its own long cycle logic, all arriving at consequential points in their respective trajectories simultaneously.

Which is precisely what the series as a whole has been building toward. The economic picture is not the whole picture. But it is now complete enough that the convergence, when we name it fully, will have the weight it deserves.

Next: Why communication revolutions precede structural transitions, and why the current one is different from all the ones that came before it.